New space: the reshaping of a whole industry

30 May 2020, 19:22 UTC: the Falcon 9 Rocket onboarding Crew-Dragon Demo-2 is launched. SpaceX is about to become the first private entity to send humans in orbit. This event is representative of the reshaping of the space market occurring since the beginning of the 21st century and sharply accelerating in recent years.

Historically, states took a prominent position in this industry, but private companies are now entering. They are becoming major actors of the space sector, collaborating with established state players at every stage of the value chain: launchers, satellites, infrastructures, and services. This new paradigm opens new possibilities for companies to create value, they are now driving force of projects and missions, more than simple stakeholders, with an essential objective: profitability. This has led to a total disruption of the technologies used: reusable or micro launchers and CubeSats are facilitating access to space, which has never been so affordable.

A new generation of launchers, the symbol of new space

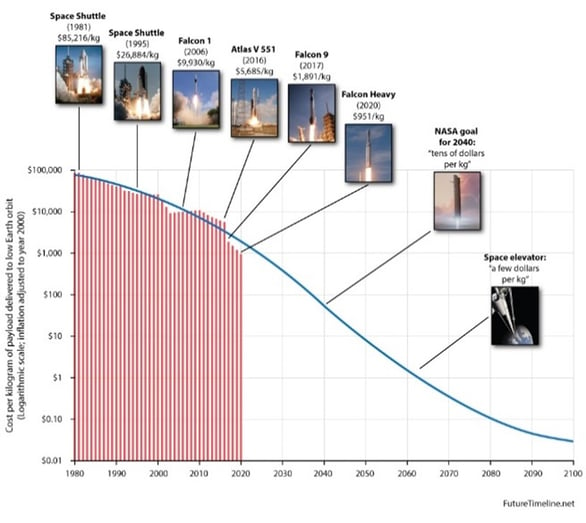

Indeed, launchers have always been emblematic of the space industry in the mainstream culture, the symbol of the power of a country and its ability to access space: Saturn V, Space Shuttle and Soyuz are today emblematic names. It is also true nowadays, specifically about SpaceX which has been very mediatized for its reusable launchers, currently used by the NASA to transport astronauts to ISS, and to put a diversity of satellites in orbit. In this field, SpaceX is in a way the symbol of many private newcomers, which have in common a low-cost model, to offer an access to space or linked services at a reduced price.

The concept of partially or fully reusable launcher is not new. It was already the case of the Space Shuttle, which aimed at reusing the Orbiter Vehicle, for cost saving reasons. As we know the intended goal failed, costs never came below those of expendable launch systems, in addition to safety issues that resulted in tragic incidents. Where the Space Shuttle failed, SpaceX succeeded, and this revolution is due to the convergence of different factors. Firstly, the low-cost policy comes from a private actor, with a profitability objective, that makes a major difference compared to a project initiated by a public entity. Secondly, it is combined to a technological leap that allowed a safe and efficient reuse of some part of the launcher.

since the 80s but broken with the new generation of reusable launchers

Source: FutureTimeline.net$

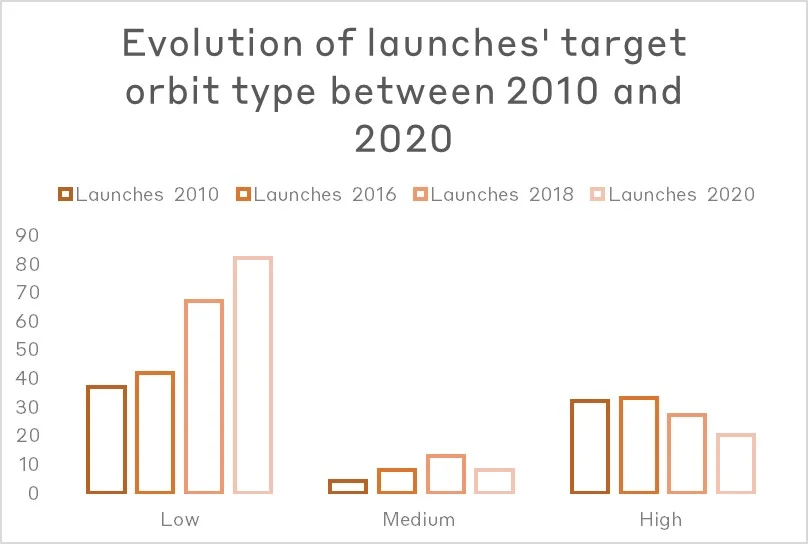

And in the end, the Low Earth Orbit payload cost per kilogram drastically decreased with those new launchers. According to some estimations, it could be divided by 2 with a Falcon Heavy compared to a Soyouz, or a Falcon 9 compared to an Ariane 5. As a consequence, a virtuous circle is initiated, with the costs decreasing, the demand increases, as well as the number of missions. Indeed, 2020 has been a first-of-its-kind year, with a total of 114 launches including 10 fails, an unattained number since the Soviet bloc collapse and the beginning of the second space age. It is also important to note the strong increase of Low Earth Orbit launches in the past decade, particularly for 5 years: +95% between 2016 and 2020, while the number of high earth orbit (GEO, GSO) slightly decreases.

in past decade, especially since 2016

The easier and cheaper access to space leads to an increasing demand for spatial services: this is the third factor of the convergence favouring the emergence of new private actors. In this context, new micro launchers are also developed, the latter require lower development and operation costs compared to heavy ones and are able to answer to the changing demand for smaller satellites that are now becoming a new standard.

Reshaping the satellite market: the CubeSat revolution

At the same time, the market is reshaped by the size and weight reduction of satellites. The apparition of small satellites, and more specifically CubeSats, is possible thanks to electronics miniaturization, and motivated by launch cost reduction goal of private companies. This corresponds to the same transformation mechanism than launchers: the combination of private newcomers and technological leap. In addition to the weight reduction, the emergence of CubeSats allows a design standardisation of satellites, with the creation of a new unit corresponding to the volume of one CubeSat (10cm x 10cm x 10cm), equivalent to an approximate weight of 1kg. Indeed, a small sat can be composed of an assembly of several CubeSats, its volume being a multiple of this unitary value: 1U, 2U, 3U… Miniaturization and standardization enable mass-production with a facilitated industrialization encouraged by the use of off-the-shelf components. To sum up, satellites are now cheaper and easier to produce with shorter lead times, opening access to space to minor actors for which it was not possible up to now, such as universities.

The average price for the manufacturing and launch of a CubeSat is approximately USD 150 000 on average but can drop down to $50 000(1). In the same time, the capital expenditure for deploying a GEO satellite (manufacturing, launch, insurance and gateway station) is estimated from $150 million to $500 million(2). Even if these figures are only estimations, don’t necessarily include the same service, and are to be viewed cautiously in absolute, there is more than a factor 1000 between LEO and GEO estimation costs.

This logically favours the increase of number of satellites sent in orbit: 1272 in 2020, which is an absolute record and representing a +120% increase in comparison to 2019. Within this context, LEO constellations of nanosatellites (weight from 1kg to 50kg, generally conform to CubeSat norm) made their apparition. They are capable to ensure the same service compared to a classical GEO satellite, with more resilience and flexibility. These constellations enable new actors to accomplish various applications, and new ways to create value. At this pace, and if the model of constellations is validated, 16000 LEO satellites are to be launch before 2025.

New players, new applications

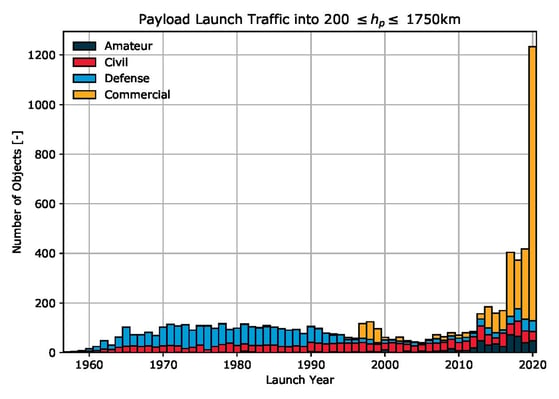

As discussed in the previous parts, space is now easier and cheaper to access, which allows new players initiatives in various applications. Indeed, we notice an unprecedent increase of commercial missions, that has been initiated since the beginning of the 2010s, boosted by the emergence of new needs to serve spatial applications.

Source: ESA’s Annual Space Environment Report 2021

For example in Earth Observation, sun-synchronous orbit (an orbit in which the satellite is synchronized with the sun’s path) is appreciated, because for any point on the earth, the illumination angle of the sun will be the same. In this case, a constellation of small satellites can provide a worldwide daily updated imaging of any zone of the planet. The fact that small satellites are less costly to produce and to launch facilitates this initiative, in addition to the fact that a given satellite of the constellation is readily replaceable if required.

This is also transposable to telecommunication applications, that are taking advantage of this change in paradigm. The most known initiatives are Starlink, from SpaceX once again, Kuiper (Amazon) and OneWeb. They are completed by new players such as Inmarsat who recently announced their Orchestra constellation project, and multiple smaller data relay initiatives. Until today, internet access through GEO satellites encountered difficulties to established itself against on ground solutions such as fibre networks or 4G-5G mainly because of insufficient throughput and high latency. Now LEO constellations offer a steady opportunity to solve the problems GEO satellites encountered while bringing new proposition, such as an easy access to internet worldwide, even in the most isolated areas without the need of building a heavy infrastructure.

Conclusion

New space refers to an ecosystem modification caused by the combination different factors that are mutually dependent: technological disruptions for launchers and satellites, entry of new actors, new ways of creating value in space. All of them are supporting each other, for example the entry of new actors participating to the disruption and cost decreasing, and the other way around. It is also leading to a shift in stakeholders and activities, with an increasing part of private players and the emergence of new countries. More than a replacing of state actors by young companies, the space landscape seems to move in a way where legacy public actors, large private aerospace structure and new young companies collaborate to shape the new age of space.

All these satellites need to communicate, between themselves and with the earth. Data is essential, and the transmission tool is then very strategic. Different ways of doing it coexist, the conventional one is using radio frequency, and is used since the beginning of space exploration, but optical transmission using laser is also making its apparition since a few years. This will be discussed in the next feature article of The New Space Times.

(1) « Space Is Open For Business, Online » , sur Rocket Lab

(2) Geostationary satellite orders bouncing back – SpaceNews

By Julien Bayol

Julien Bayol holds a Master’s degree in mechanics from INSA and has completed a Master’s degree in Management at Toulouse Business School. Very interested in advanced manufacturing techniques, through the use of innovative optical solutions, Julien is assistant product manager at Cailabs. He contributes to the development and commercialization of CANUNDA and TILBA® products.